How to Get Equipment Financing for Your Startup

(Even Without Business History)

Securing equipment financing for startup business ventures is one of the biggest challenges entrepreneurs face today. Unfortunately, most lenders expect your business to be operational for at least one year , creating a frustrating catch-22 situation for new companies.

We understand this struggle all too well. Without a good credit history, it's hard to get financing. Without financing, cash flow is tight, and not enough cash makes it difficult to grow . Despite these challenges, startup equipment financing options do exist. In fact, some equipment lenders may provide funding to small-business owners with personal credit scores in the 500s , although most recommend a score of at least 650 .

Are you worried about your startup's limited business history or less-than-perfect credit score? Don't be discouraged. Even if traditional banks seem hesitant, alternative financing paths are available for your heavy equipment financing needs. Many startups have successfully secured equipment loans for startup business growth without the lengthy track record lenders typically prefer.

In this guide, we'll explore how to overcome the common obstacles to equipment financing with bad credit or limited business history, and share strategies that have helped thousands of new businesses get the tools they need to succeed.

Why Startups Struggle to Get Equipment Financing

Starting a business involves numerous financial hurdles, but getting equipment financing may be among the most frustrating. Data shows the stark reality facing new ventures—up to 90% of startups fail overall, with 10% failing in the first year and a staggering 70% closing their doors between years two and five [1]. These sobering statistics create a challenging environment for securing the necessary funding.

Lack of business credit history

New businesses face an immediate disadvantage when seeking equipment financing. Without an established track record, lenders have limited information to assess creditworthiness. For small-ticket equipment leasing—typically transactions under $100,000—lenders often focus more on the business owner's personal credit profile than on the business itself [2].

Furthermore, business credit scores examine several factors that startups simply haven't had time to build: payment history with lenders, credit utilization, length of business operation, and public records like liens or bankruptcies [3]. This chicken-and-egg problem leaves many entrepreneurs struggling to qualify for their first equipment loans.

Cash flow limitations in early stages

Cash flow challenges compound financing difficulties for new ventures. Startups frequently operate with tight margins and unpredictable revenue streams, making regular loan payments difficult to guarantee.

Unfortunately, equipment purchases often require substantial capital at the precise moment when cash reserves are most precious. Without financing options, startups must choose between delaying essential equipment purchases or depleting working capital needed for daily operations [4]. Seasonal businesses face additional pressure, as their ability to make consistent monthly payments may not align with their irregular income patterns [5].

High risk perception by lenders

From the lender's perspective, startups represent significant risk. Traditional financing institutions rely heavily on credit scores and business history when evaluating loan applications [6]. A recent industry report found that 60% of small businesses cited access to financing as their top challenge [7].

Consequently, startups often face higher costs when they do qualify for financing. These may include elevated interest rates, personal guarantee requirements, stricter terms, shorter lease durations, higher fees, or limited upgrade options [2]. This risk premium makes equipment acquisition more expensive precisely when new businesses can least afford additional costs.

How Equipment Financing Helps Startups Grow

Equipment financing serves as a strategic growth engine for new ventures, offering advantages that extend well beyond simply acquiring machinery. Nearly 8 in 10 U.S. companies use some form of equipment financing rather than outright purchases [8], demonstrating its value across industries.

Preserves working capital

The primary benefit of equipment financing for startup businesses lies in capital preservation. Instead of depleting cash reserves for expensive equipment purchases, entrepreneurs can spread costs over manageable monthly payments. This approach allows startups to maintain liquidity for critical operational needs like marketing, product development, and unexpected expenses.

Notably, some financing options can cover up to 125% of the equipment's upfront cost, providing additional funds for transportation, installation, training, and maintenance [9]. These "extras" typically add 25-30% to equipment costs [9], making financing particularly valuable for cash-conscious startups.

Enables access to essential tools

Equipment financing provides immediate access to productivity-enhancing tools without large initial investments. For startups in manufacturing, healthcare, construction, or technology sectors, this means beginning operations with state-of-the-art equipment rather than waiting until sufficient capital accumulates.

This accessibility creates a significant competitive advantage. Modern equipment can replace manual work, boost productivity, and reduce operational costs [9]. Moreover, financing options like leasing offer flexibility for technology that requires frequent updates, helping startups stay current with industry innovations [9].

Builds business credit over time

Perhaps the most overlooked long-term benefit is credit building. Regular, timely payments on equipment financing help establish a positive business credit profile [10]. This credit history becomes increasingly valuable as startups grow, potentially leading to more favorable financing terms for future needs.

Equipment loans are particularly effective for credit building since they're generally easier to qualify for than unsecured financing options. According to the Federal Reserve Banks' 2024 Small Business Credit Survey, 68% of auto or equipment loan applications received full approval—the highest rate among all loan types [11]. The equipment itself serves as collateral, making lenders more comfortable extending credit to businesses with limited operating history.

How to Qualify for Startup Equipment Financing

Qualifying for equipment financing as a new venture requires preparation and strategy. While traditional lenders typically require at least one year in business and $50,000 in annual income [12], startups can still secure funding by following specific steps.

Organize financial documents

Initially, compile essential paperwork to strengthen your application:

Income Statement: Shows your business's profitability

Balance Sheet: Details your assets, liabilities, and equity

Bank Statements: Demonstrates cash flow patterns

Tax Returns: Validates your financial health [12]

Having these documents organized beforehand speeds up the application process and creates a positive impression that might lead to better financing terms [13].

Improve personal credit score

Most equipment financing requires a personal credit score of at least 650 [12]. However, some lenders may consider applications with lower scores if you can demonstrate solid cash flow over the past three to six months [12]. To boost your score, pay bills on time, keep credit utilization low, and regularly monitor your credit reports for errors [14].

Offer collateral or a co-signer

The equipment itself typically serves as built-in collateral, making these loans more accessible for those with less-than-perfect credit [15]. Additionally, providing extra collateral like property or other equipment can further secure the financing [16]. Alternatively, adding a co-signer with strong credit may help you qualify and potentially secure better interest rates [16].

Create a strong business plan

A well-crafted business plan effectively communicates your goals to lenders [17]. Include detailed projections showing how the equipment will generate revenue [18]. Your plan should address key questions: Will the business generate sufficient cash flow? What products/services will you sell? What markets will you target? How will you manage risk? [17]

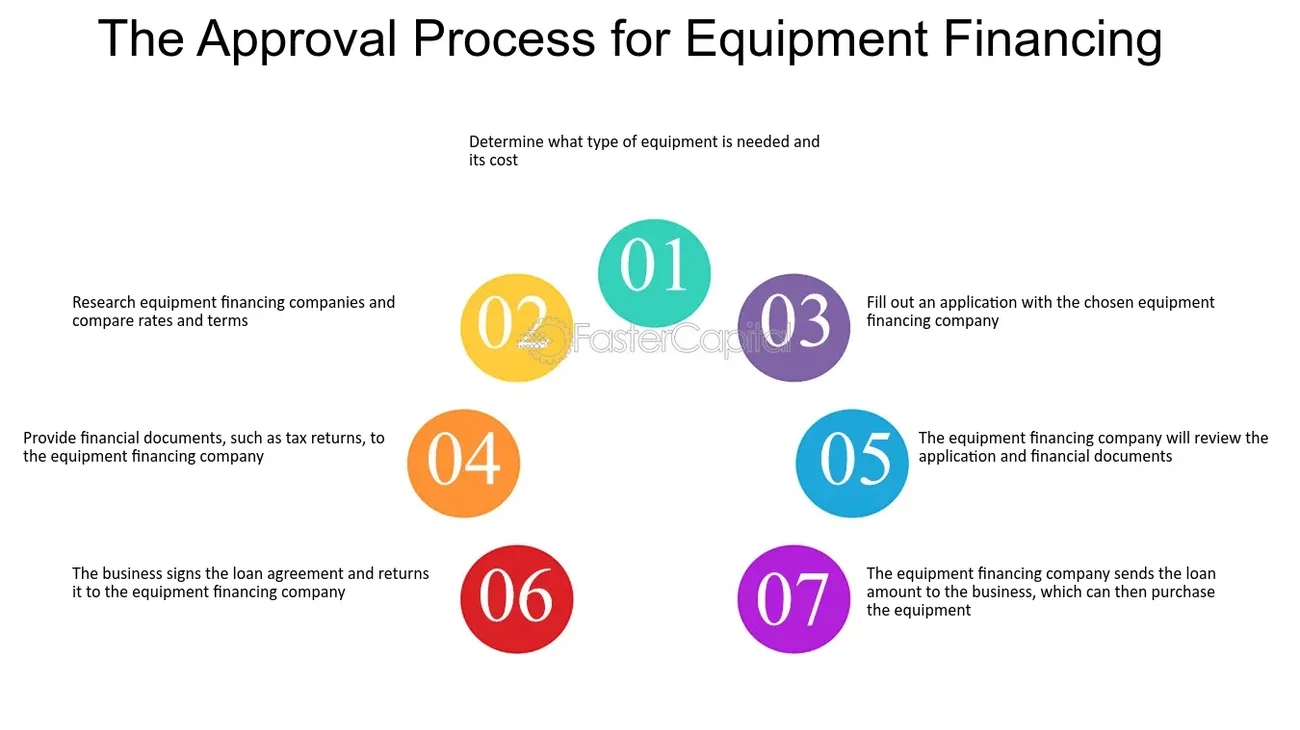

Best Places to Get Equipment Loans for Startups

Image Source: FasterCapital

Finding the right funding source can make all the difference for startups needing equipment without established business history. Each option offers unique advantages depending on your specific situation.

Online lenders with flexible terms

Online lenders typically offer faster approvals and more flexible requirements than traditional banks. Companies like National Funding approve applications within 24 hours and require only six months in business and $250,000 in annual sales [19]. Similarly, OnDeck provides funding with just one year in business and $100,000 annual revenue [19]. Cardiff stands out by offering equipment financing without conducting hard credit checks on your personal score [19].

SBA-backed loan programs

SBA loans remain among the most affordable options for startups. The 7(a) loan program—SBA's primary business loan program—covers equipment purchases up to $5 million with guarantees of 85% for loans under $150,000 [20]. Essentially, SBA 504 loans require as little as 10% down payment [21], making them accessible for cash-strapped startups.

Vendor financing and lease-to-own options

Approximately 57% of all equipment acquisitions are financed through loans, leases, or lines of credit, with leasing being the most common method (26% of acquisitions) [22]. Vendor financing allows businesses to purchase equipment directly from manufacturers or suppliers who provide the financing themselves. This arrangement benefits both parties—vendors increase sales while customers access products without immediate full payment [22].

Top equipment financing companies for startups

Beacon Funding specializes in startup equipment financing with 70% of businesses approved within 24 hours [23]. For startups requiring minimal annual revenue, iBusiness Funding offers loans up to $500,000 with only $50,000 in annual revenue requirements [24].

Ready to secure equipment financing for your startup? Submit a form to get matched with our lending partners who can provide the financing you need.

Conclusion

Equipment financing presents a viable path forward for startups despite the traditional barriers of limited business history and credit challenges. Throughout this guide, we've seen that even new ventures can access the tools needed for growth without depleting precious working capital. Additionally, making regular payments on equipment loans helps build the business credit profile necessary for future financing opportunities.

Certainly, the financing landscape might seem intimidating at first glance. Nevertheless, the strategies outlined above—organizing financial documents, improving personal credit scores, offering collateral, and creating strong business plans—significantly increase approval chances. Alternative options like online lenders, SBA-backed programs, and vendor financing make equipment acquisition possible even for companies in their earliest stages.

Remember that equipment financing isn't merely about acquiring assets; it's about positioning your startup for sustainable growth while maintaining cash flow flexibility. Most successful businesses use some form of equipment financing rather than outright purchases for this exact reason. Take the next step in growing your startup. Submit a form today to match with our lending partners and get the equipment financing your business needs.

Above all, don't let limited business history discourage you from pursuing the equipment your startup needs. With the right approach and financing partner, your business can overcome the catch-22 of needing equipment to grow but lacking the history to finance it. Start exploring these options today—your startup's growth potential depends on having the right tools at the right time.

References

[1] - https://www.beaconfunding.com/blog/article/category/equipment-financing-101/can-a-startup-get-equipment-financing

[2] - https://www.experian.com/blogs/small-business-matters/2025/05/19/how-strong-business-credit-can-help-you-secure-better-equipment-leases/

[3] - https://www.bannerbank.com/financial-resources/blog/your-business-credit-score-matters-heres-why

[4] - https://sallyportcf.com/equipment-financing-for-startups-the-lowdown/

[5] - https://www.biz2credit.com/equipment-financing/equipment-financing-mistakes-to-avoid

[6] - https://www.linkedin.com/pulse/startup-equipment-financing-navigating-challenges-vkn6c

[7] - https://directcreditfunding.com/unlock-your-startups-potential-equipment-financing-solutions-with-direct-credit-funding/

[8] - https://www.pnc.com/insights/corporate-institutional/raise-capital/the-benefits-of-equipment-financing.html

[9] - https://www.bdc.ca/en/articles-tools/money-finance/get-financing/equipment-financing-101-everything-you-need-know

[10] - https://www.beaconfunding.com/businesscredit

[11] - https://www.bankrate.com/loans/small-business/pros-cons-of-equipment-loan/

[12] - https://www.nationalfunding.com/blog/grow-with-equipment-financing/

[13] - https://firstbusiness.bank/resource-center/financial-statements-to-secure-equipment-financing/

[14] - https://apfinancing.com/2023/09/tips-on-improving-personal-and-business-credit-score/

[15] - https://www.unitedcapitalsource.com/blog/business-credit-bad-personal-credit/

[16] - https://www.nerdwallet.com/article/small-business/no-credit-check-equipment-financing

[17] - https://www.farmcreditofvirginias.com/blog/do-i-need-business-plan-get-loan

[18] - https://www.beaconfunding.com/blog/article/category/equipment-financing-101/equipment-financing-for-start-up-business

[19] - https://www.cnbc.com/select/best-equipment-financing-options/

[20] - https://www.sba.gov/funding-programs/loans/7a-loans

[21] - https://blp504.org/unlocking-equipment-financing-solutions-with-sba-504/

[22] - https://www.nfscapital.com/vendor-financing/

[23] - https://beaconfunding.com/equipment-financing/financing-programs/start-up-financing

[24] - https://www.bankrate.com/loans/small-business/best-equipment-business-loans/

Here’s the Real Truth About Grants and Smarter Ways to Fund Your Business

Arizona Business Owners: Here’s the Real Truth About Grants and Smarter Ways to Fund Your Business

Let’s be honest: everyone wants a $10,000 grant to start a small business in Arizona. And why not? Free money sounds like the ultimate win. But if you’re betting everything on that, you might be wasting time you could be using to actually build your business.

Grants are real. But they’re limited, competitive, and usually come with strings attached. So here’s how to really approach funding your business, and yes, I’ll still give you the best places to look for free grants to start a business in Arizona.

How Can I Get a Grant for My Business in Arizona?

Start with local resources. You’ll be surprised how many small opportunities are available once you know where to look:

Arizona Commerce Authority – Their Small Business Services page often shares local and state grant programs.

Local Chambers of Commerce – From Phoenix to Tucson, many Chambers run seasonal microgrant programs or partner with city development agencies.

Arizona Community Foundation – Offers grant funding across different industries and counties.

Maricopa SBDC & Local Economic Development Offices – Many of these teams maintain grant and business funding directories or offer support applying for programs.

National Grant Competitions Open to Arizonans – Like the FedEx Small Business Grant, Visa’s She's Next Grant Program, or Comcast RISE.

You can also use tools like grants.gov or HelloAlice.com and narrow the filters by geography and industry.

Why Grants Aren’t Enough (And What You Should Do Instead)

Here’s the thing, if you spend all your energy chasing grants, you might miss out on actually building momentum. Even if you’re applying for every program out there, it could take 6–12 months to see anything happen.

Meanwhile, your business could be making money, if you had a little capital to get it moving.

That’s where I come in. If you’re serious about launching or scaling your business in Arizona, you need a solid plan and real money to back it.

Start Here: Build a Business Plan

The first thing anyone will ask, whether it’s a grant reviewer, investor, or lender, is this:

“What’s your plan?”

You need a business plan with:

Clear goals

Financial projections

How you’ll use any funding

A timeline for growth

This gives you the confidence to talk about your business and gives lenders confidence to work with you.

Real Arizona Funding Options That Don’t Rely on “Free Money”

Here’s what most successful small businesses do:

1. Raise a Small Round from Friends or Family

Just be transparent. Share your business plan and show where every dollar will go.

2. Apply for a Business Loan Online (Yes, Even in Early Stages)

I work with a network of trusted lenders and I help Arizona entrepreneurs every day get access to:

SBA loans (including SBA 7(a) loans)

Easy approval startup business loans

Term loans

Business lines of credit

Invoice factoring

Equipment financing

ERC advances

Merchant cash advances

And yes, many of these can fund as fast as the same day.

Apply once, and I’ll match you to the best lender based on your business profile. No stress. No hidden fees. Just the funding you need.

Ready to Start?

If you're ready to stop Googling “how can I get grant for my business in Arizona” and start actually building, here’s what to do:

Fill out our short intake form so I can help get you matched.

Download our PDF with all loan product options we refer to.

Or just reach out with your business idea—we’ll talk through it.